DisInterested

Math Helps Me Know Where to Direct My Rage

Let’s talk about greed. Specifically: the greed that is interest on home mortgage loans.

As with many things, this blog post is inspired by a tweet. This time, it is my own:

If you’re really interested, you can take a look at the thread on Twitter, but the TLDR of it is that I wanted to break down the cost of the loan to the person. The most standard mortgage loans are 15 year and 30 year loans, so that’s what I focused on with The Math.

Why?

Notably, the reason I was even doing the math was because of a completely different issue: balancing out my budget with popular budget software You Need A Budget or YNAB:

Screenshot of YNAB Twitter page on 24 July 2021.

Screenshot of YNAB Twitter page on 24 July 2021.

YNAB has a feature where you reconcile what the software reports your balance as being vs what the balance actually is. This can be the balance of any asset or liability that the platform either 1 ) allows you to import or 2 ) manually create. So for your bank accounts, credit cards, and so forth YNAB does the sums and subtractions to determine your current balance from your previous balance. If you had $50, spent $25, YNAB reports your current balance as $25. Straightforward, right?

I noticed that the “reconciliations” for my credit card and banking accounts were accurate, so A+ to them on that. I noticed they were very off for the types of loans I have that use compound interest. Loans that commonly use compound interest are student loans and mortgages, as well as some other types of loans because why not make this more pervasive rather than less. I realized the loan amounts were off by precisely the amount they would have been if it were not for compound interest. Cue twitter thread.

Intro to Home Mortgage Math

Photo by Joss Woodhead on Unsplash

Photo by Joss Woodhead on Unsplash

Why were the results incorrect for compound interest? Because the math isn’t direct there and they’d need more data than I saw inputs for in order to do those calculations. If you’ve been exposed to student loans, mortgages, etc. you’ve likely seen what is called an “amortization table”. If not, let’s introduce you to this joy right now:

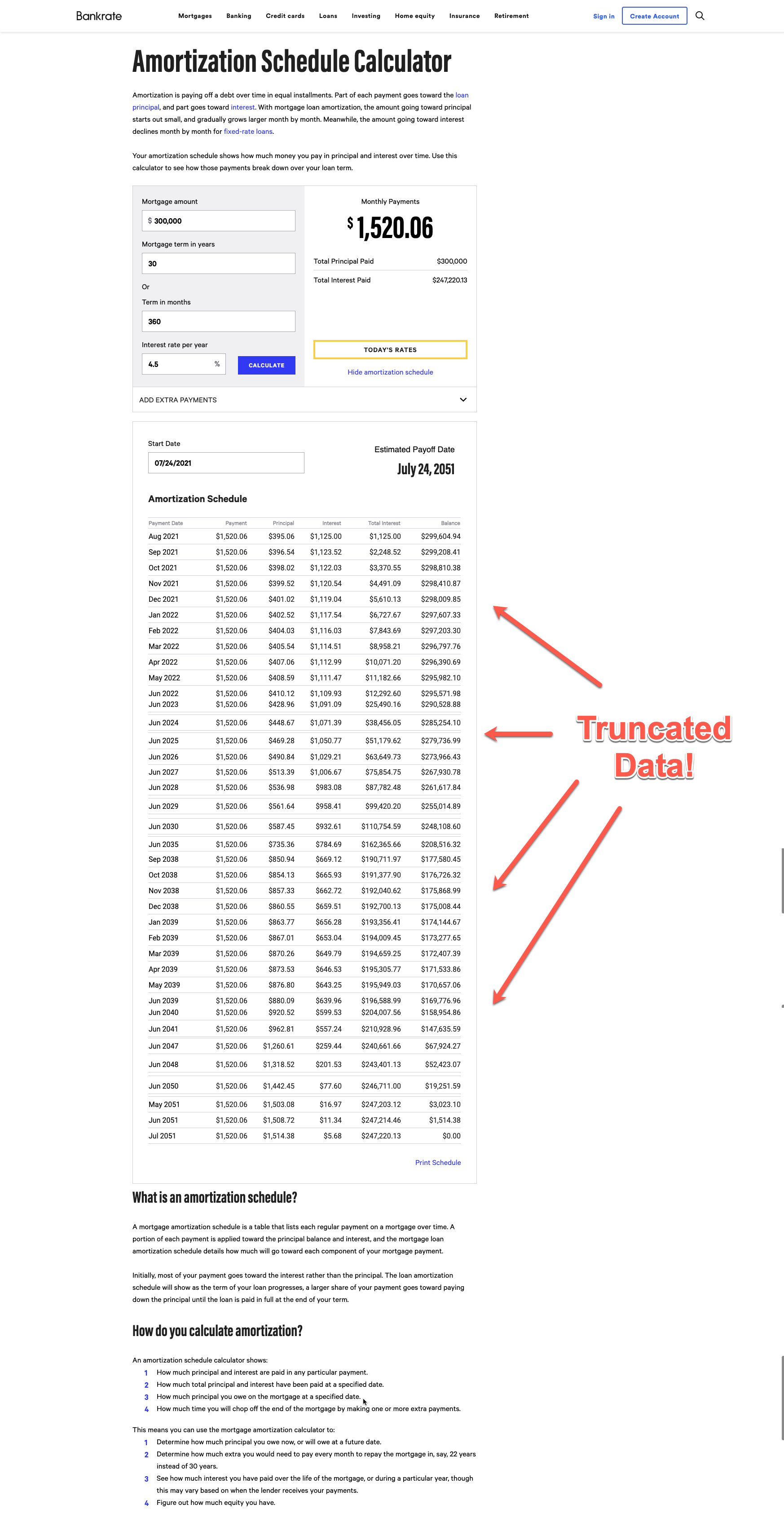

Source: Bankrate’s Amortization Schedule Calculator with starting inputs of $300,000, 30 years, and 4.5% interest.

Source: Bankrate’s Amortization Schedule Calculator with starting inputs of $300,000, 30 years, and 4.5% interest.

Due to the size of that, you can either click on the image to see it full size or you can go to the source and put in the same inputs:

- $300,000 loan

- 30 years / 360 months

- 4.5% interest

Amoritization tables typically spell out the payment every single month because of That Whole Compound Interest Thing. What this shows is that the monthly payment is the same for all 30 years, in this case $1520.06, but that the money is allocated differently every month. Specifically, that money is split into paying off what’s called the principal, i.e. the loan itself, and the interest. In your first loan payment on this schedule in August 2021 you’ll pay $1520.06 but only $395.06 pays down the principal, a whopping $1125.00 pays the interest. To break this out a little more:

- First payment, August 2021:

- Payment: $1520.06

- Principal: $395.06

- Interest: $1125.00

- Middle(ish) payment about 14 years in, June 2035:

- Payment: $1520.06 (still)

- Principal: $735.36

- Interest: $784.69

- Last payment, Jul 2051:

- Payment: $1520.06 (still)

- Principal: $1514.38

- Interest: $5.68

In case you are asking:

What does that mean for me?

Basically, if you take out a loan for $300,000 your first payment reduces that to $299,604.94. If the full $1520.06 went toward the principal, then it’d be $298,749.94. This is also the reason that the amoritization schedule has a “total interest” and “balance” column - when you look at that June 2035 date you can see in this scenario you would’ve paid:

- $162,365.66 in interest

- $208,516.32 is the remaining on principal

- Putting this another way, you’ve paid off $91,483.68 of that $300,000 loan.

- TLDR you’ve paid ~$71k more in interest than toward the loan.

On the other hand, if 100% of those $1520.06 payments had gone toward principal, then your balance at this point would actually be about $44,629.92 and you’d be nearly done.

Instead, you’re about 15 years into a 30 year loan and you’ve paid more on interest than on the loan.

What Special Hell Is This?

This is compound interest. This is why a calculator like (what I assume) YNAB uses struggles with finding the “true balance” for a compound loan. The payoff of the original loan isn’t linear, so YNAB would need to know the start date, duration, and if you’re making any additional payments on the principal in addition to the interest rate to be able to generate a table like this and actually calculate the true remaining balance of your loan.

For the interested, the formula for compount interest looks like this:

(Present value) x ( 1 + (interest rate))(Number of periods) = (Future value)

Simple interest, like sales tax, is actually just the case where “Number of periods” is 1, as in you pay the whole amount including interest in one payment. This is common for things like sales tax. If you have $50 in goods for groceries, and you live in an area with 8.75% sales tax, then you’d have:

$50 x (1 + 0.0875)1 = ~$54.35 (with rounding)

For a loan like a mortgage, the “number of periods” is monthly. So for a 30 year loan, it’s 360 periods. That’s why the monthly value is always there, and why the amoritization schedule displays the way it does. If the number of periods were per year instead, it would drastically impact the calculation as you’d have 30 periods instead of 360.

Ok But Why Aren’t The Payments 50-50?

Photo by Gabriel Meinert on Unsplash

Photo by Gabriel Meinert on Unsplash

Basically, if the monthly payment is $1520.06, why doesn’t $760.03 go to the principal and interest at the same time?

Short answer: greed.

If you look at the amoritization table, at the end you will have paid off the $300,000 loan as well as $247,220.13 in interest. By top loading the interest in this way:

- You pay 50% of the compound interest in the first 10 years of the loan, but only 20% of the loan.

- It will take you 20 years, or 2/3rds the life the loan, to pay off 50% of the loan prinicipal.

- In that time you will have paid off approximately 85% of the interest.

This of course has implications for your next home purchase. It’s very common to sell a house to buy another house. To avoid exceeding the scope of this post to a side post about housing inflation, if after 10 years you sell your house for as much as you bought it for, you “get” 20% and then the remaining 80% pays off the remainder of your loan. In a different pay schedule you’d have more money, but the bank would have less, and we can’t have that now can we?

Just to be perfectly clear: there is no scenario where the banks don’t make an absolute fuck ton of money off of you as a borrower, no matter how they organize the schedule.

Why My Twitter Math was Off

I started the tweet storm with the value of $300k because when I did a quick search on median home value in the United States, the result was about $280k and $300k was just a rounder number for more straightforward mental math. Instead of using a simple amoritization schedule calculator like here, though, I used a “Mortgage Calculator”. The idea with a mortgage calculator is that it usually calculates the total monthly payment but not just on the mortgage itself. There are other factors that go into your total monthly payment when you own a house in the United States. You pay property taxes every year, you might have Private Mortgage Insurance (or PMI), homeowner’s insurance, as well as HOA fees and so on. So a mortgage calculator takes all of these into account.

When you get a home loan in the United States the “default” assumption is that you “need” to provide a 20% payment. For the language of the loan itself, that means that if the house is $300k, the down payment is $60k, and the actual loan is $240k. The reason for the 20% “assumption” is because if you put less than 20% down, you get hit with what’s called Private Mortgage Insurance. The extreme summary of this is that you are considered “more risky” by having less cash to pay at purchase, so they charge you more money elsewhere. PMI does not go toward your loan or its interest. The reason behind the PMI is to protect the lender of the loan, the bank, if the borrower cannot make payments. Since the money they’re getting off the compound interest is clearly not enough to make ends meet, they pass that cost on to you as the borrower.

Depending on the calculator, it might automagically add in the PMI to the monthly payment if you enter in a down payment less than 20%. So when I was calculating how much interest someone would pay over the life off the loan, scaling out the extra payment for all 360 cycles (for a 30 year loan) or 180 cycles (for a 15 year loan) caused incorrect results. Not that the bank isn’t still royally screwing you, just to be clear.

Updated Math

To keep this part brief, if you purchase a $300,000 house and looking at the mortgage only:

- 20% down, 3.5%, 30 year

- Monthly Payment: $1077.71

- Total Interest Paid: $147,974.61

- Loan + Interest Paid: $387,974.61

- 20% down, 3.5%, 15 year

- Monthly Payment: $1715.72

- Total Interest Paid: $68,829.26

- This is about half the interest paid in the 30 year scenario.

- Loan + Interest Paid: $308,829.26

The wealthier, and thus less risky, you are the lower the interest rate you are going to get. If you’ve had too much life happen before you apply for a home loan, your wealth is lower, your credit score is lower, your debt-to-income ratio less favorable, and your interest rate higher. Let’s boost the above to 4.0%, which is just 0.5% higher:

- 20% down, 4.0%, 30 year

- Monthly Payment: $1145.80

- Total Interest Paid: $172,486.82

- Loan + Interest Paid: $412,486.82

- This is $24,512.21 more than the 3.5% scenario

- 20% down, 4.0%, 15 year

- Monthly Payment: $1775.25

- Total Interest Paid: $72,545.18

- Loan + Interest Paid: $312,545.18

- This is $4,301.83 more than the 3.5% scenario

Let’s say you put 15% down so you can reserve more cash in case your home surprises you in its first year - repairs and so on. I won’t be including the PMI here, but this now breaks down to:

15% down, 3.5%, 30 year

- Monthly Payment: $1145.06

- Total Interest Paid: $157,223.02

- Loan + Interest Paid: $412,223.02

- This is $15,263.80 more than the {20% down, 3.5%, 30 year} scenario

- 5% of $300k, the value of the house, is about $15k. So while you kept the cash for your runway, you do end up paying it to the bank.

15% down, 3.5%, 15 year

- Monthly Payment: $1822.95

- Total Interest Paid: $73,131.09

- Loan + Interest Paid: $328,131.09

- This is $4,301.83 more than the {20% down, 3.5%, 15 year} scenario

15% down, 4.0%, 30 year

- Monthly Payment: $1217.41

- Total Interest Paid: $183,267.24

- Loan + Interest Paid: $438,267.24

- This is $26,044.22 more than the {20% down, 3.5%, 30 year} scenario

15% down, 4.0%, 15 year

- Monthly Payment: $1886.20

- Total Interest Paid: $84,516.72

- Loan + Interest Paid: $339,516.72

- This is $11,385.63 more than the {20% down, 3.5%, 15 year} scenario

How To Help You

Even just skimming those figures, you can see that the main way the banks make money off of you is by playing the long game. The lower payments of the 30 year vs 15 year loans in each scenario is not very much in the scheme of things, but definitely enough to be felt by you as a borrower, banks can double or so the amount of money they take from you. It’s also worth mentioning that 15 year loans and 30 year loans typically have different interest rates. That said, the 15 year interest rates do tend to be lower than the 30 year interest rates. So you might find yourself qualifying for either a 30 year 4.0% loan or a 15 year 3.5% loan, just to limit to the info above for quick comparisons on potential implications.

Mentally Model Loans Like Goods for Purchase

You might have limited bargaining power for how much you can push back on how this system works, but you can use some knowledge about how it works to help yourself. This can help you shift your mindset from solely “the banks are fucking me over, I hate everything” (which, yes, they are) to “I am purchasing a loan”. If you have the {20% down, 3.5%, 30 year} scenario above you are “purchasing a loan for about $150k”. If you do the 15 year scenario, you are “purchasing a loan for about $70k”.

Basically you need to evaluate your finances to figure out not only How Much House Can I Afford but also How Much Loan Am I Willing to Afford.

Of course with the caveat of what the banks are willing to offer you. If you can afford to shorten your loan, and your goal is to pay the banks less money, then you should definitely be aiming for the shorter loans. You can see this holds true even if the interest rate ends up higher for the 15 year loan: in the above scenario the {20% down, 4.0%, 15 year} loan has ~$73k in interest vs the {20% down, 3.5%, 30 year} loan’s ~$150k in interest.

Briefly Explaining PMI

There are also other things that can help you to know, for example I will take a moment to mention PMI. You only pay PMI until the value of the loan is 80% of the purchase price. So if you put 15% down, then the loan is for 85% of the value of the home. You will pay the PMI until it is 80%. BUT! Another systemic factor: by top loading paying off interest and not principal it takes you longer to pay that 5% down. In the {15% down, 3.5%, 30 year} scenario it’ll take you about 3 years to pay down that 5%. You will have paid about $26,000 in interest in that time.

Another gotcha with PMI: some (most?) banks require you to notify them when you hit that 80%, otherwise they will continue to charge you for longer. Specifically for 2% extra, so the PMI will automatically stop at 78% instead of 80%. In the {15% down, 3.5%, 30 year} scenario the bank will get about two extra years of PMI from you thanks to that top loaded interest schedule. To drive this point home a little further: if you have 10% down in the {3.5%, 30 year} scenario it’ll take you 6 years to hit 80% and about another year for the 78%.

Strategize

Photo by Daniel Thiele on Unsplash

Photo by Daniel Thiele on Unsplash

When you make a purchase, like a house or a car, you probably plan on focusing a lot of energy into the actual object you are purchasing. What type of house is a home? What is easy to fix (paint) vs difficult to fix (foundational issues, water damage)? And so on.

Thanks to capitalism, you can give the banks the same level of scrutiny. It does make sense, because again you’ll be purchasing a $300,000 home with a $150,000 loan (substitute with your own actual numbers). Knowing what to consider will help you strategize.

Shop Around And Be Transparent About It

In America there are probably as many brick-and-mortar banks as churches. The process is exhausting but you’ll want to make sure that you’re using the fact that these banks want your money to point them at each other. Remeber: this is the short game for you, the long game for them. Expanding on earlier examples:

$300,000 house, 20% down, 30 year means a loan of $255,000 and:

- At 3.5%

- $1,145.06 per month is your payment

- $157,223.02 total interest

- At 3.7%

- $1,173.72 per month is your payment

- $167,539.78 total interest

- This is about $10,000 more than the previous, and is only 0.2% higher interest

Putting this in terms of “things home needs”, depending on the size of your house this is a roof or a partial roof, heater, hot water tank, and so on. This is money that can pay down or off remaining balances on student loan debt or medical debt. Basically: all real money. Don’t view any money that goes into the interest as a “wash”.

Deploy capitalistic toxic competition to your advantage. If someone is offering you 0.1% lower tell another bank that’s so. If they counter with 0.1% lower than that, tell the other bank and so on. Fight them down. To them $157k is still better than $0, and to you $157k is better than $167k.

Also make sure to compare loan terms. e.g. If one bank has an early pay-off penality (… capitalism …), then depending on how severe that is you might want to trade it off with a higher interest loan that gives you the ability to pay off early if you reasonably expect to be able to do so.

Have A Basic Understanding of Your Debt-to-Income

I definitely recommend reading at least one, dedicated, blog post on Debt-to-Income. The reason it’s important to understand is that banks use this, in addition to your credit score and Trade Secrets™️, to figure out those loan terms. Anything that a bank uses is something you need to understand in order to use for defense.

The main thing I want you to take away here is that being able to adjust your debt-to-income ratio as much as is in your personal power can potentially save you and your family a lot of money. Make sure to discuss with a financial advisor* to fully grok any other downstream effects (… capitalism …), but know this:

- Loans are designed so that your monthly payment is the same.

- That monthly payment is based on the original value of the loan.

- Therefore tricks like refinancing those loans, which changes the original value to a new loan to be whatever the current balance is, or directly paying down the principal in advance of your home loan, will shift your debt-to-income to being more in your favor.

- Notable call out, this may impact your credit score, which is why, again, you should make sure you’re talking to someone* to understand the downstream effects for you personally.

If you’re not sure how far off your debt-to-income is from whatever threshold they are looking at, ask. That’s what I had to do, and then I looked at my existing debt to see if there was a way to move numbers around (paying more on this, less on that) to get it down to below threshold by enough. In order to do that I needed the information of what “enough” was.

* - For financial advisors. I know many people do not have one, heck I don’t have one, but it’s entirely likely that you have access to one through your employer especially if they have 401k / 403b plans, RSUs / options, etc. available as benefits. Make sure to check your benefits to see if this applies to you.

Absolutely Fuck PMI

Based on NerdWallet, PMI ranges from 0.58% to 1.86% of the original loan amount. So for the $300,000 house with 15% down, you might see a PMI of $106 (using NerdWallet’s calculator). You’ll pay about $3,775 in PMI until you reach that sweet 80% number which is about 3 years in this example. Recalling that the PMI doesn’t automatically disappear until you reach 78%, or about 4 years, and that’s closer to $5,088. So that’s fun.

This may not seem like a lot, but it depends on whether or not you live in a high cost of living area as well. $1,000,000 is a lot of money, but if you live in the San Francisco Bay Area, close to New York City, or in similarly sized cities it won’t get you far. For a $1,000,000 residence in those areas this can quickly become an extra $413 per month and a whopping $43,089 total (calculation assumed a 1% down payment, or $10,000).

Absolutely Fuck Around with Those Amoritization Tables

Know your loan terms and do some best guesses on ways you can get that loan down further. I know I’ve said it over and over in this post, but this is absolutely the bank’s playground. There are consequences for being late on mortgage payments that can have longer term impacts on your finances than just the risk of losing your home, as if that isn’t bad enough. But starting to think of what “paying on principal, early” can mean for you can help.

For example, let’s say you are looking at the {20% down, 3.5%, 30 year} loan that I outlined waaaay above. That monthly payment is $1,145.06. The monthly payment for the {20% down, 3.5%, 15 year} loan is $1,822.95. If you get the 30 year loan, and add $677.89 to your monthly payment, your 30 year loan does become a 15 year loan - you pay it off early. (Remember to look for those early payoff penalties I mentioned earlier to see if those exist and how they will impact you.) Why not just get the 15 year loan? There are reasons. Perhaps you didn’t qualify for reasons out of your control, that definitely happens. But you might also find yourself considering that sometime in the length of the loan you’ll need to have smaller mortgage payemnts. You can do this by refinancing as well, or if you get the longer loan you can stop paying the extra against principal until you’re in a better situation, putting the ball slightly more in your court.

There are more and different ways that you can see how different payments impact your loan schedule. You can see how monthly extra payments on principal vs annual payments can impact the interest you’re paying on your loan. If you’re looking at making annual payments instead of monthly, make sure you shift around what month you apply it (there’s a reason the calculator asks) so you can see how much it impacts the interest across the life of the loan.

Different Types of Loans and What Do You Qualify For

And last but not least, know that there are different types of home loans. When you start your loan applications, make sure to apply for the different types of loans you might qualify for. Bankrate has an article about these, but to summarize their summary there are conventional loans, fixed rate or adjustable rate, government loans, and “jumbo mortgages”. This latter is most common in high cost of living areas, as there are federal loan limits for home price. Government issued loans includ FHA, USDA, and VA loans. The first two are intended for people who are low-to-moderate income, don’t have a high credit score, etc. and the last is specifically for veterans of the United States military.

Resources

If you want to toggle around with a PMI calculator, NerdWallet has a good one here.

The Bankrate Amortization Schedule / Calculator is here. This is the same one linked above.

NerdWallet, in general, has a lot of articles about mortgages here.

Make sure you read up on early payoff penalties, here’s an article to get you started (same as linked in text of post).

Something I didn’t cover here, that is important, is that there are different types of loans. A quick review of what else to consider when figuring out your mortgage is here.

Cover image photo by Michelle Phillips on Unsplash